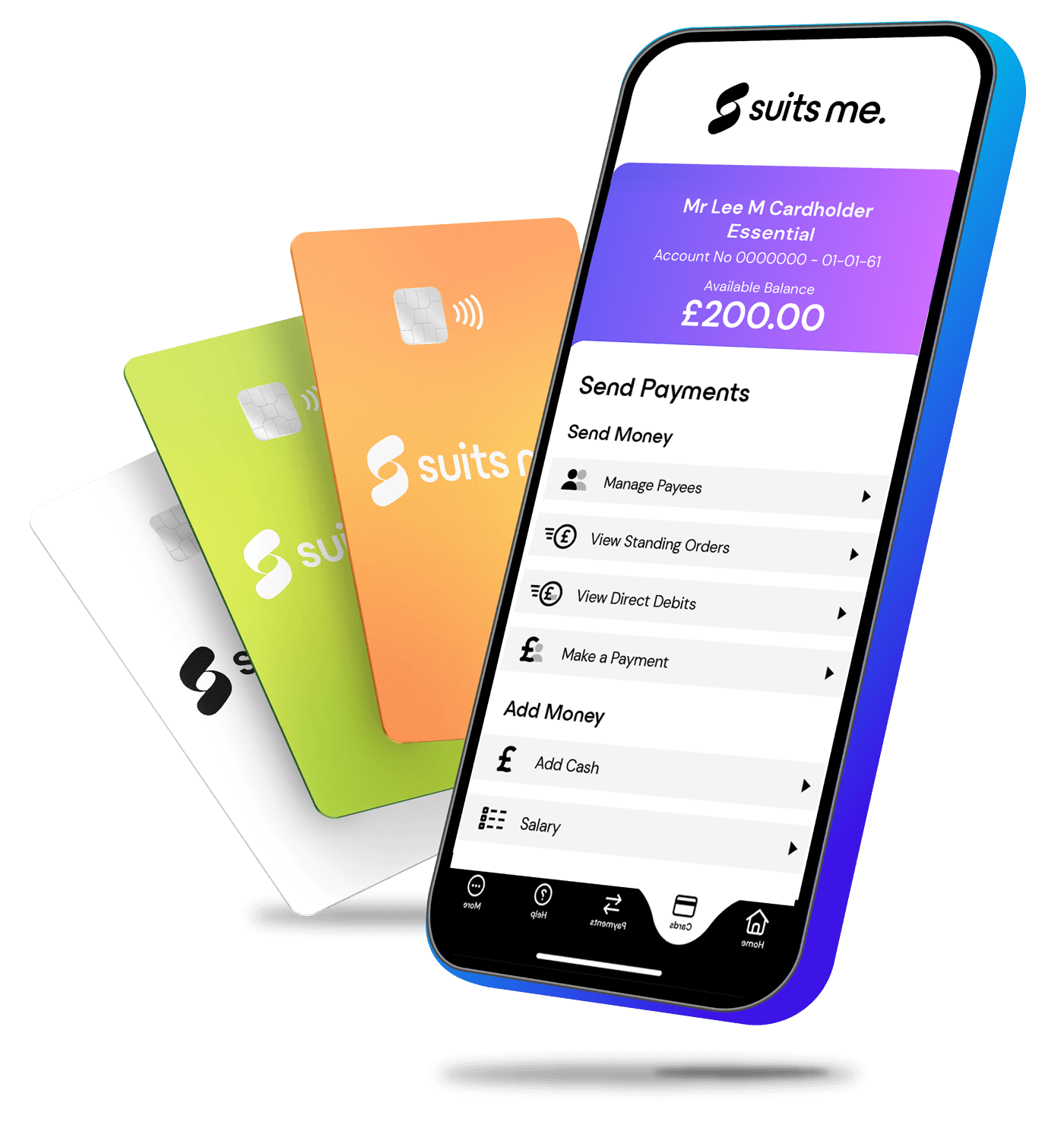

Debt Management Plan DMP and need an account?

If you’re entering into or are in a Debt Management Plan (DMP), we provide instant personal accounts in minutes.

✅ Instant sort code & account number

✅ Easy online application

✅ Suitable if you’ve been rejected by bank

If you’re entering into or are in a Debt Management Plan (DMP), we provide instant personal accounts in minutes.

✅ Instant sort code & account number

✅ Easy online application

✅ Suitable if you’ve been rejected by bank

Staying Organised While Repaying Debt

One of the biggest challenges during debt management is staying organised.

Many people find it helpful to:

- Separate repayment money from everyday spending

- Track essential bills carefully

- Avoid additional borrowing

- Use structured budgeting tools

Having clear systems in place can reduce stress and help you stay consistent with repayments. No matter what type of debt product you have entered into, it could be an IVA, Bankruptcy or Debt Relief Order, organising your money with a separate account gives you the best chance to re start your finances.

Some people using a Debt Management Plan may also have struggled with other forms of debt or insolvency. If you’re looking for information related to bankruptcy, you can learn more about opening a banking account for bankruptcy.

Why Open an Account With Suits Me

when you have a Debt Management Plan?

Amazing features & benefits with every Suits Me account

Payments and transfers

Receive and send money in the UK and send money abroad easily. Have wages or benefits sent directly to your account, send a Faster Payment or cash top up at any PayPoint store.

Cashback as standard

Save money when you use your Suits Me card in our partner retail stores or when you shop online. You’ll get cashback back into your Suits Me account.

Discounts with top brands

Access our exclusive customer discounts with top brands. We have different partners every week for you to enjoy great money-off deals.

24/7 access

Instant access to your account wherever, whenever, via the online portal on our website or with the Suits Me app.

Refer a friend

Refer your friends to apply and use their Suits Me card, and earn up to £50 per friend! No limit on the number of friends you refer.

Account holder competitions

Join in our exclusive account holder competitions every month for the chance to win cash prizes, amazing discounts and much more.

Thousands of people

trust Suits Me

-

I’ve been struggling to get work without a bank and suits me have gave me a chance they have been brilliant so far thanks.

Nathan Noon, Suits Me customer

-

The best bank to be with. This app, and this bank, it’s keeping in touch with you 24/7, and it’s solving your issues in seconds. I very very recommend it!

Julia, Suits Me customer

-

So far so good. Had an issue with my previous bank. Suits Me stepped in and provided everything I needed in a very stressful time. Very happy to keep using them to receive my money and spend it,especially in shops like IKEA 😌

Jack, Suits Me customer

-

Hello! Thank you accepting me and giving me a chance to live, to work, to carry on with my existence! I was very impressive about your promptitude giving me answer to my question! Thanks!***

LC, Suits Me customer

-

This was my last chance and I am glad go have a banking account, suits me is a life saver, ok you have to pay for some transactions but it is not much, but it is worth it.

Michael Emm

-

Fantastic, the best bank service I’ve ever had.

Jack, Suits Me customer

-

I love this little bank. A great card – easy access to online – great support team.

Tamara, Suits Me customer

-

Brilliant bank so far.

Craig, Suits Me customer

1

1

Choose an account

Select your account type and complete the online application in 3 minutes.

Add Funds to Your Account

Add money via transfer, wages or cash topup.

3

3

Use Suits Me Everyday

Get cashback on your everyday shopping.

Choose the right account for you

Essential

Back Up Account

Pay as you go /month

-

If you already have a main bank account and want a back-up personal account that’s easy to open and use, this account is perfect for you. For occasional monthly spending with a pay-as-you-go flexible card and mobile app. If you are doing more than a handful of transactions each month our other accounts may be better for you.

-

If you already have a main bank account and want a back-up personal account that’s easy to open and use, this account is perfect for you. For occasional monthly spending with a pay-as-you-go flexible card and mobile app. If you are doing more than a handful of transactions each month our other accounts may be better for you.

Premium

Spending Account

£5.97 /month

-

For everyday spending you get more for your money with this account. If you are making regular transfers and drawing out cash, Premium will be a good choice. Cashback, discounts, and everything you need to spend with ease.

-

For everyday spending you get more for your money with this account. If you are making regular transfers and drawing out cash, Premium will be a good choice. Cashback, discounts, and everything you need to spend with ease.

Premium Plus

Main Account

£9.97 /month

-

If you need an account for your wages and benefits, setting up regular payments or somewhere to pay cash in, Premium Plus is the best choice. Enjoy full benefits, VIP phone queue jump, and maximum rewards. The ideal hassle-free alternative to a high-street bank for your main account.

-

If you need an account for your wages and benefits, setting up regular payments or somewhere to pay cash in, Premium Plus is the best choice. Enjoy full benefits, VIP phone queue jump, and maximum rewards. The ideal hassle-free alternative to a high-street bank for your main account.

Who is a debt management plan suitable for?

A DMP is typically suited to people who have a regular income but are finding it difficult to meet minimum monthly payments across multiple debts. It works best for unsecured debts and is generally considered when debts are manageable enough not to require a more formal insolvency solution like an IVA or bankruptcy.

How long does a debt management plan last?

The length of a DMP depends on the total amount owed and what you can realistically afford to repay each month. Most plans last between one and ten years, though some people complete theirs sooner if their financial situation improves or they receive a lump sum to settle debts early.

Will a debt management plan affect my credit score?

Yes. A DMP will typically have a negative impact on your credit score, as you are repaying debts at a reduced rate rather than meeting the original agreed terms. This information stays on your credit file for six years. However, for many people, the improvement in financial stability outweighs the short-term impact on their credit rating.

Do I need to switch bank accounts when starting a debt management plan?

It is strongly recommended that you open a new bank account before your DMP begins. If you bank with an institution you also owe money to — such as an overdraft or credit card with the same bank — they have the legal right to use funds in your current account to offset what you owe them. This is known as the right of set-off, and it can leave you without money for essential living costs.

What should I look for in a bank account when on a debt management plan?

You’ll want an account with no overdraft facility, no credit products attached, and no links to any of your existing creditors. Ideally it should support direct debits and standing orders so you can manage your regular bills and DMP payments smoothly. Accounts that don’t require a credit check are also worth looking for, as your credit score is likely to be affected during a DMP.

Can I still open a bank account with bad credit during a DMP?

Yes. A number of providers offer accounts specifically designed for people with poor credit histories. These are sometimes called basic bank accounts bank account alternatives like Suits Me. They typically don’t run credit checks, so your DMP or credit score won’t prevent you from being accepted.

Will switching bank accounts affect my debt management plan?

No. Switching to a new bank account does not interfere with your DMP itself. Your DMP provider will continue to manage your repayments as agreed. You will simply need to update your employer with your new account details for wages, and update any direct debits or standing orders to your new account.

Can creditors still contact me or charge interest during a DMP?

A DMP is an informal agreement, so creditors are not legally obliged to freeze interest or stop contacting you. However, many creditors will agree to do so once a plan is in place. A reputable DMP provider will negotiate on your behalf to try to get interest and charges suspended.

Should I use a free or paid DMP provider?

Free DMP providers such as StepChange and Citizens Advice offer the same service as paid providers at no cost to you. Using a free provider means more of your money goes towards repaying your debts rather than fees. It is generally recommended to use a free, FCA-regulated provider.