План за управление на дълговете ( DMP ) и се нуждаете от профил?

Ако се включвате в план за управление на дългове (DMP) или вече участвате в такъв, ние ви предоставяме лични сметки за минути.

✅ Незабавно получаване на код на банката и номер на сметка

✅ Лесно онлайн кандидатстване

✅ Подходящо, ако сте били отхвърлени от банка

Ако се включвате в план за управление на дългове (DMP) или вече участвате в такъв, ние ви предоставяме лични сметки за минути.

✅ Незабавно получаване на код на банката и номер на сметка

✅ Лесно онлайн кандидатстване

✅ Подходящо, ако сте били отхвърлени от банка

Как да поддържате ред, докато изплащате дълговете си

Едно от най-големите предизвикателства при управлението на дълговете е да се поддържа ред.

Много хора смятат, че е полезно да:

- Отделете парите за погасяване на дългове от тези за ежедневни разходи

- Следете внимателно основните си сметки

- Избягвайте да теглите допълнителни заеми

- Използвайте инструменти за структурирано бюджетиране

Наличието на ясни системи може да намали стреса и да ви помогне да спазвате графика за погасяване. Независимо от вида на дълговия продукт, по който сте сключили договор – било то индивидуално доброволно споразумение (IVA), фалит или заповед за облекчаване на дългове – организирането на парите ви чрез отделна сметка ви дава най-добрия шанс да възстановите финансовото си състояние.

Някои хора, които използват план за управление на дълговете, може да са се сблъсквали и с други форми на дългове или неплатежоспособност. Ако търсите информация, свързана с фалита, можете да научите повече за откриването на банкова сметка при фалит.

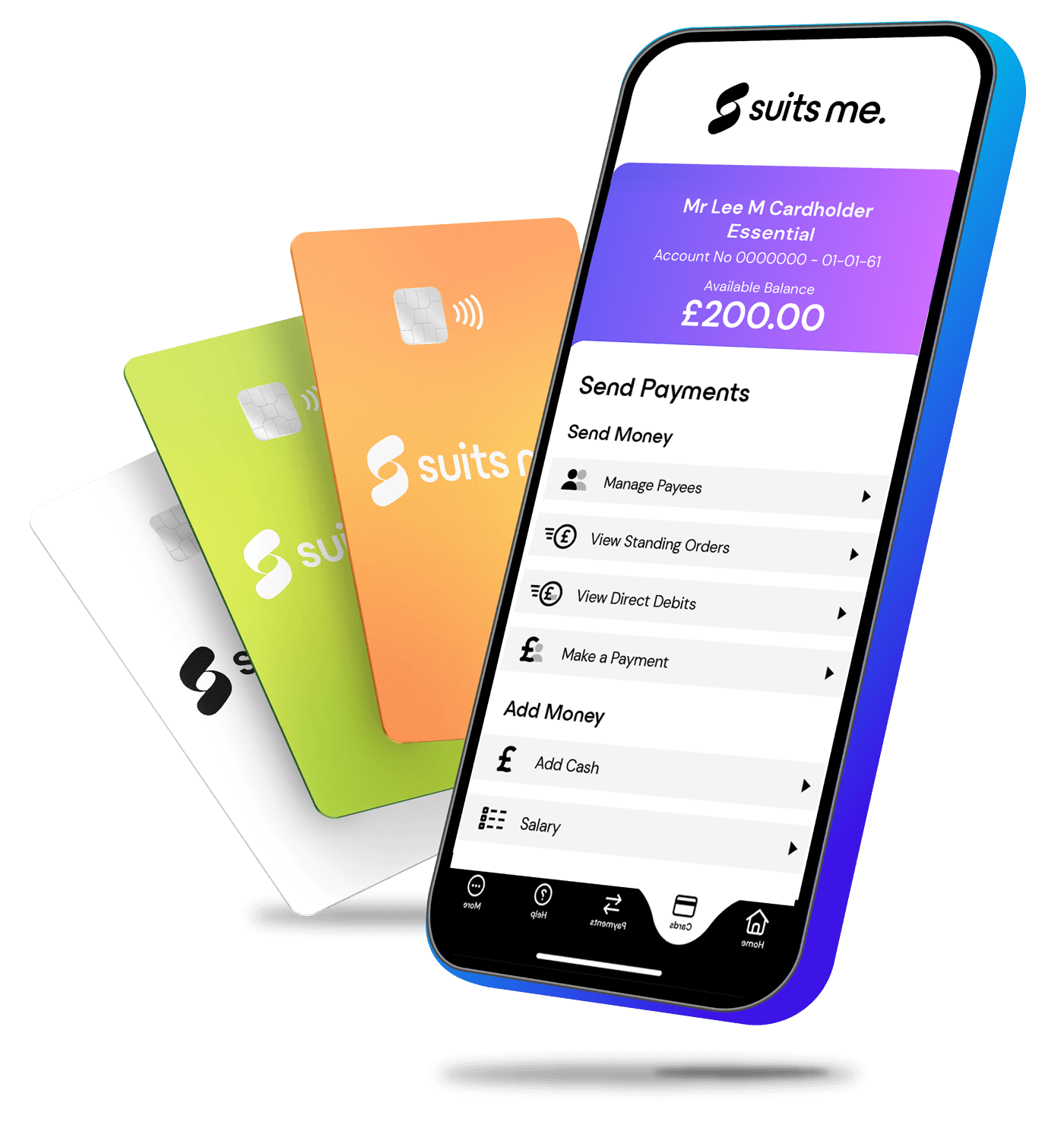

Защо да си откриете сметка в Suits Me

когато имате план за управление на дълговете?

Невероятни функции и предимства с всеки акаунт в Suits Me

Плащания и трансфери

Получавайте и изпращайте пари в Обединеното кралство и изпращайте пари в чужбина лесно. Изпращайте заплатите или обезщетенията директно по сметката си, изпращайте бързи плащания или превеждайте пари в брой във всеки магазин на PayPoint.

Възстановяване на парични средства като стандарт

Спестете пари, когато използвате картата си Suits Me в нашите партньорски магазини или когато пазарувате онлайн. Ще получите обратно пари в сметката си за Suits Me.

Отстъпки с най-добрите марки

Получете достъп до нашите ексклузивни отстъпки за клиенти с най-добрите марки. Всяка седмица имаме различни партньори, с които можете да се насладите на страхотни оферти с отстъпка.

Денонощен достъп

Незабавен достъп до профила ви от всяко място и по всяко време чрез онлайн портала на нашия уебсайт или с приложението Suits Me.

Препоръчай приятел

Препоръчайте на приятелите си да кандидатстват и да използват картата Suits Me и спечелете до £50 на приятел! Няма ограничение за броя на препоръчаните от Вас приятели.

Конкурси за титуляри на сметки

Присъединете се към нашите ексклузивни конкурси за притежатели на сметки всеки месец, за да спечелите парични награди, невероятни отстъпки и много други.

Хиляди хора

доверие ми подхожда

-

Имах трудности да си намеря работа, без да имам банкова сметка, но „Suits Me“ ми дадоха шанс и досега се справят чудесно – благодаря им.

Натан Нун, клиент на Suits Me

-

Най-добрата банка, с която да работите. Това приложение и тази банка поддържат връзка с вас 24/7 и решават вашите проблеми за секунди. Много, много го препоръчвам!

Джулия, клиент на Suits Me

-

Дотук всичко е наред. Имах проблем с предишната си банка. Suits Me се намеси и ми предостави всичко, от което се нуждаех в един много стресиращ момент. Много се радвам, че продължавам да ги използвам, за да получавам парите си и да ги харча, особено в магазини като IKEA 😌

Джак, клиент на Suits Me

-

Здравейте! Благодаря ви, че ме приехте и ми дадохте шанс да живея, да работя и да продължа да съществувам! Бях много впечатлен от бързината, с която отговорихте на въпроса ми! Благодаря!***

LC, клиент на Suits Me

-

Това беше последният ми шанс и се радвам, че вече имам банкова сметка – за мен това е истинско спасение. Да, трябва да плащаш за някои транзакции, но сумата не е голяма, а си струва.

Майкъл Ем

-

Фантастично, най-доброто банково обслужване, което съм получавал.

Джак, клиент на Suits Me

-

Обичам тази малка банка. Страхотна карта – лесен достъп до онлайн услуги – отличен екип за поддръжка.

Тамара, клиент на Suits Me

-

Досега банката е страхотна.

Крейг, клиент на Suits Me

1

1

Избор на профил

Изберете типа на профила си и попълнете онлайн заявлението за 3 минути.

Добавете средства към сметката си

Добавете пари чрез превод, заплати или кеш допълване.

3

3

Използвай Suits Me Everyday

Получете кешбек при ежедневното си пазаруване.

Изберете правилния акаунт за вас

Етерични

Резервен акаунт

Плащайте, както вървите /месец

-

Ако вече имате основна банкова сметка и искате резервна лична сметка, която е лесна за откриване и използване, тази сметка е идеална за вас. За спорадични месечни разходи с гъвкава карта с предплатена услуга и мобилно приложение. Ако извършвате повече от няколко транзакции всеки месец, другите ни сметки може да са по-подходящи за вас.

-

Ако вече имате основна банкова сметка и искате резервна лична сметка, която е лесна за откриване и използване, тази сметка е идеална за вас. За спорадични месечни разходи с гъвкава карта с предплатена услуга и мобилно приложение. Ако извършвате повече от няколко транзакции всеки месец, другите ни сметки може да са по-подходящи за вас.

Премия

Сметка за разходи

5,97 £/месец

-

За ежедневните разходи с тази сметка получавате повече за парите си. Ако правите редовни преводи и теглите пари в брой, Premium ще бъде добър избор. Кешбек, отстъпки и всичко, от което се нуждаете, за да харчите с лекота.

-

За ежедневните разходи с тази сметка получавате повече за парите си. Ако правите редовни преводи и теглите пари в брой, Premium ще бъде добър избор. Кешбек, отстъпки и всичко, от което се нуждаете, за да харчите с лекота.

Премиум плюс

Основна сметка

£9,97 /месец

-

Ако ви е необходима сметка за заплатата и социалните ви добавки, за да настроите редовни плащания или за да депозирате пари в брой, Premium Plus е най-добрият избор. Насладете се на пълни предимства, VIP обслужване по телефона и максимални награди. Идеалната алтернатива на традиционните банки за вашата основна сметка, без никакви усложнения.

-

Ако ви е необходима сметка за заплатата и социалните ви добавки, за да настроите редовни плащания или за да депозирате пари в брой, Premium Plus е най-добрият избор. Насладете се на пълни предимства, VIP обслужване по телефона и максимални награди. Идеалната алтернатива на традиционните банки за вашата основна сметка, без никакви усложнения.

Отворете профила си в Suits Me днес!

Открийте сметката си за по-малко от 3 минути!

За кого е подходящ планът за управление на дълговете?

Програмата за управление на дълговете (DMP) обикновено е подходяща за хора, които разполагат с редовен доход, но изпитват затруднения да покриват минималните месечни вноски по няколко дългове. Тя дава най-добри резултати при необезпечени дългове и обикновено се разглежда като вариант, когато дълговете са достатъчно управляеми, за да не се налага по-формално решение за несъстоятелност, като доброволно споразумение за дългове (IVA) или фалит.

Колко време трае планът за управление на дълговете?

Продължителността на плана за управление на дълговете зависи от общата дължима сума и от това, каква сума реално можете да си позволите да изплащате всеки месец. Повечето планове са с продължителност от една до десет години, макар че някои хора ги приключват по-рано, ако финансовото им състояние се подобри или ако получат еднократна сума, с която да погасят дълговете си предсрочно.

Ще се отрази ли планът за управление на дълговете върху кредитния ми рейтинг?

Да. Програмата за управление на дълговете (DMP) обикновено оказва отрицателно влияние върху кредитния ви рейтинг, тъй като изплащате дълговете си по намалена ставка, вместо да спазвате първоначално договорените условия. Тази информация остава в кредитната ви история в продължение на шест години. За много хора обаче подобряването на финансовата стабилност надделява над краткосрочното влияние върху кредитния им рейтинг.

Трябва ли да сменя банковата си сметка, когато започвам план за управление на дълговете?

Настоятелно се препоръчва да си откриете нова банкова сметка, преди да започне вашата програма за управление на дълговете (DMP). Ако ползвате услугите на банка, към която имате задължения — например овърдрафт или кредитна карта в същата банка — тя има законното право да използва средствата по вашата разплащателна сметка, за да компенсира сумата, която ѝ дължите. Това се нарича право на прихващане и може да ви остави без средства за покриване на основните разходи за издръжка.

На какво трябва да обърна внимание при избора на банкова сметка, когато съм включен в програма за управление на дългове?

Ще ви е необходима сметка без възможност за овърдрафт, без свързани кредитни продукти и без връзки с някой от настоящите ви кредитори. В идеалния случай тя трябва да поддържа директен дебит и постоянни нареждания, за да можете безпроблемно да управлявате редовните си сметки и плащанията по плана за управление на дълговете (DMP). Също така си заслужава да потърсите сметки, за които не се изисква проверка на кредитоспособността, тъй като кредитният ви рейтинг вероятно ще бъде засегнат по време на DMP.

Мога ли да си отворя банкова сметка, ако имам лоша кредитна история, докато съм в програма за управление на дълговете (DMP)?

Да. Редица доставчици предлагат сметки, специално предназначени за хора с лоша кредитна история. Те понякога се наричат „основни банкови сметки“ или „алтернативи на банковите сметки“, като например Suits Me. Обикновено те не извършват проверка на кредитоспособността, така че вашият план за управление на дълговете (DMP) или кредитният ви рейтинг няма да ви попречат да бъдете одобрени.

Ще се отрази ли смяната на банковата сметка на плана ми за управление на дълговете?

Не. Преминаването към нова банкова сметка не се отразява на самата програма за управление на дълговете (DMP). Доставчикът на услугата DMP ще продължи да управлява вашите плащания според договореното. Просто ще трябва да предоставите на работодателя си новите данни за банковата сметка, по която да ви се превежда заплатата, и да актуализирате всички директни дебити или постоянни нареждания, като ги пренасочите към новата сметка.

Могат ли кредиторите да продължат да се свързват с мен или да начисляват лихви по време на програмата за управление на дълговете?

Програмата за управление на дълговете (DMP) е неформално споразумение, поради което кредиторите не са правно задължени да замразят лихвите или да престанат да се свързват с вас. Въпреки това много кредитори ще се съгласят да го направят, след като планът влезе в сила. Уважаван доставчик на DMP ще преговаря от ваше име, за да се опита да постигне отлагане на лихвите и таксите.

Да избера безплатен или платен доставчик на DMP?

Безплатните доставчици на услуги за управление на дълговете (DMP), като StepChange и Citizens Advice, предлагат същите услуги като платените доставчици, без да ви струва нищо. Използването на безплатен доставчик означава, че по-голяма част от парите ви отива за погасяване на дълговете, а не за такси. Като цяло се препоръчва да се използва безплатен доставчик, регулиран от FCA.