Heb je een schuldhulpverleningsplan ( DMP ) en wil je een account aanmaken?

Als u een schuldhulpverleningsregeling (DMP) aangaat of daar al onder valt, kunt u bij ons binnen enkele minuten een persoonlijke rekening openen.

✅ Directe opvraging van bankcode en rekeningnummer

✅ Eenvoudige online aanvraag

✅ Geschikt als je door een bank bent afgewezen

Als u een schuldhulpverleningsregeling (DMP) aangaat of daar al onder valt, kunt u bij ons binnen enkele minuten een persoonlijke rekening openen.

✅ Directe opvraging van bankcode en rekeningnummer

✅ Eenvoudige online aanvraag

✅ Geschikt als je door een bank bent afgewezen

Georganiseerd blijven tijdens het aflossen van schulden

Een van de grootste uitdagingen bij schuldbeheer is om alles goed georganiseerd te houden.

Veel mensen vinden het handig om:

- Zet het geld dat je wilt aflossen apart van je dagelijkse uitgaven

- Houd essentiële rekeningen goed bij

- Vermijd extra leningen

- Gebruik gestructureerde tools voor budgettering

Het hebben van duidelijke systemen kan stress verminderen en u helpen om uw aflossingen consequent te blijven betalen. Ongeacht het soort schuldregeling dat u bent aangegaan – of het nu gaat om een IVA, faillissement of een schuldkwijtscheldingsbevel – biedt het organiseren van uw geld via een aparte rekening u de beste kans om uw financiën weer op orde te krijgen.

Sommige mensen die gebruikmaken van een schuldbeheerplan hebben mogelijk ook te maken gehad met andere vormen van schulden of insolventie. Als u op zoek bent naar informatie over faillissement, kunt u meer te weten komen over het openen van een bankrekening bij faillissement.

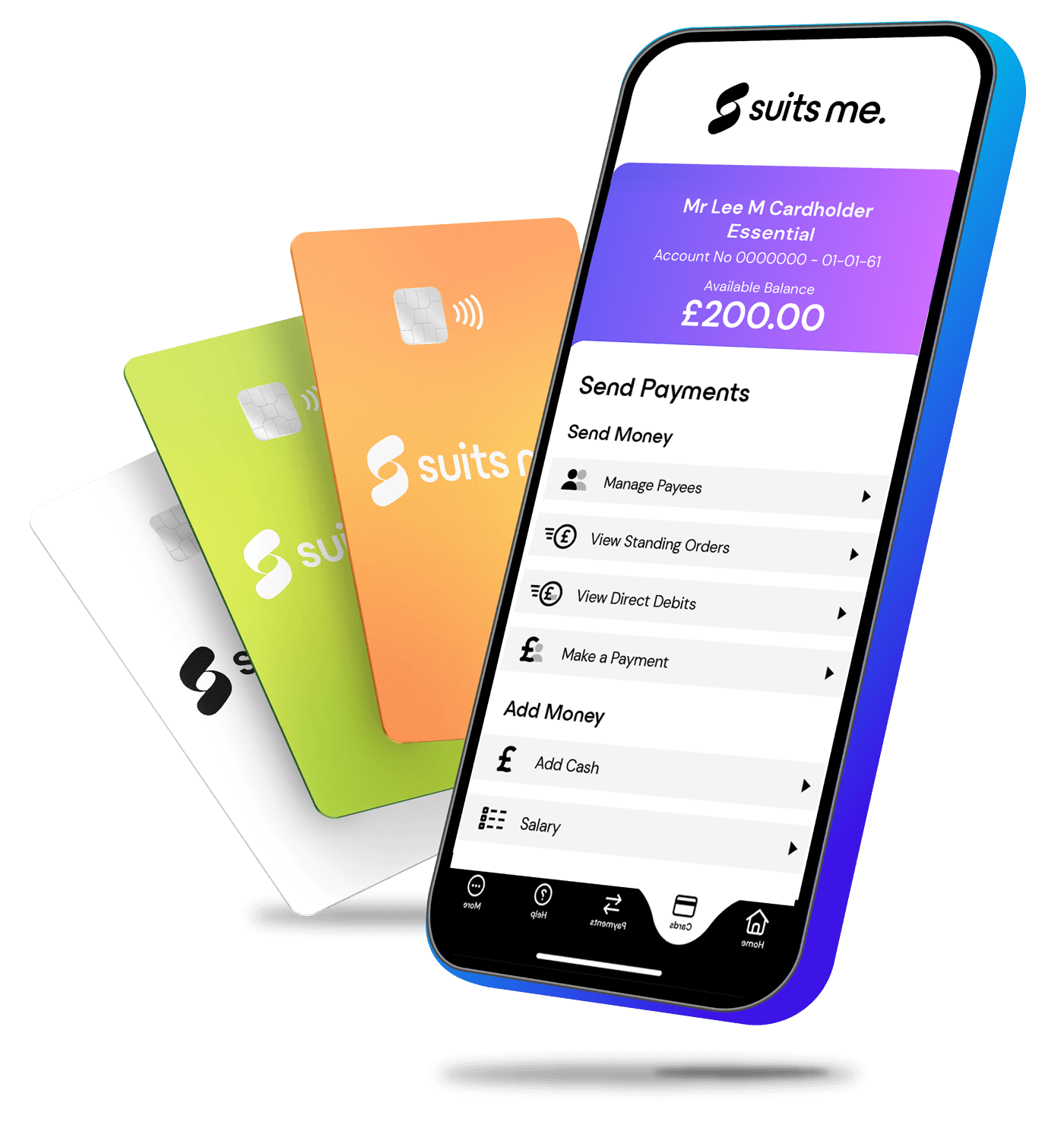

Waarom een account openen bij Suits Me?

wanneer je een schuldhulpverleningsplan hebt?

Geweldige functies en voordelen bij elk Suits Me-account

Betalingen en overdrachten

Ontvang en verstuur gemakkelijk geld in het Verenigd Koninkrijk en stuur geld naar het buitenland. Laat lonen of uitkeringen rechtstreeks naar uw rekening sturen, stuur een snelle betaling of waardeer contant geld op in een PayPoint-winkel.

Standaard cashback

Bespaar geld wanneer je je Suits Me-kaart gebruikt in onze partnerwinkels of wanneer je online winkelt. Je krijgt cashback terug op je Suits Me-account.

Kortingen bij topmerken

Krijg toegang tot onze exclusieve klantenkortingen met topmerken. Elke week hebben we andere partners zodat je kunt genieten van geweldige aanbiedingen.

24/7 toegang

Directe toegang tot je account, waar en wanneer dan ook, via het online portal op onze website of met de Suits Me app.

Verwijs een vriend

Verwijs je vrienden om hun Suits Me kaart aan te vragen en te gebruiken en verdien tot £50 per vriend! Geen limiet op het aantal vrienden dat je doorverwijst.

Wedstrijden voor rekeninghouders

Doe elke maand mee aan onze exclusieve wedstrijden voor rekeninghouders en maak kans op geldprijzen, geweldige kortingen en nog veel meer.

Duizenden mensen

Vertrouwen past bij mij

-

Ik had moeite om werk te vinden zonder bankrekening, maar Suits Me heeft me een kans gegeven. Ze zijn tot nu toe geweldig geweest, bedankt.

Nathan Noon, klant van Suits Me

-

De beste bank om bij te zijn. Deze app en deze bank houden 24/7 contact met je en lossen je problemen binnen enkele seconden op. Ik raad het ten zeerste aan!

Julia, klant van Suits Me

-

Tot nu toe gaat alles goed. Ik had een probleem met mijn vorige bank. Suits Me kwam tussenbeide en bood me alles wat ik nodig had in een zeer stressvolle periode. Ik ben erg blij dat ik hen kan blijven gebruiken om mijn geld te ontvangen en uit te geven, vooral in winkels zoals IKEA 😌

Jack, klant van Suits Me

-

Hallo! Bedankt dat jullie me hebben toegelaten en me de kans hebben gegeven om te leven, te werken en mijn leven voort te zetten! Ik was erg onder de indruk van hoe snel jullie mijn vraag hebben beantwoord! Bedankt!***

LC, klant van Suits Me

-

Dit was mijn laatste kans en ik ben blij dat ik nu een bankrekening heb; het is echt een uitkomst voor mij. Oké, je moet voor sommige transacties betalen, maar dat is niet veel, en het is het zeker waard.

Michael Emm

-

Fantastisch, de beste bankservice die ik ooit heb gehad.

Jack, klant van Suits Me

-

Ik ben dol op deze kleine bank. Een geweldige kaart – gemakkelijk online toegankelijk – uitstekend ondersteuningsteam.

Tamara, klant van Suits Me

-

Tot nu toe een geweldige bank.

Craig, klant van Suits Me

1

1

Kies een account

Selecteer uw type rekening en vul de online aanvraag in 3 minuten in.

Geld op uw rekening storten

Voeg geld toe via overschrijving, loon of contante aanvulling.

3

3

Gebruikt Suits Me Everyday

Ontvang cashback op uw dagelijkse boodschappen.

Kies de juiste rekening voor u

Essential

Back-upaccount

Betaal als je gaat /maand

-

Als u al een hoofdbankrekening hebt en een extra persoonlijke rekening wilt die gemakkelijk te openen en te gebruiken is, dan is deze rekening perfect voor u. Voor incidentele maandelijkse uitgaven met een flexibele prepaidkaart en mobiele app. Als u meer dan een handvol transacties per maand uitvoert, zijn onze andere rekeningen wellicht beter voor u.

-

Als u al een hoofdbankrekening hebt en een extra persoonlijke rekening wilt die gemakkelijk te openen en te gebruiken is, dan is deze rekening perfect voor u. Voor incidentele maandelijkse uitgaven met een flexibele prepaidkaart en mobiele app. Als u meer dan een handvol transacties per maand uitvoert, zijn onze andere rekeningen wellicht beter voor u.

Premium

Uitgavenrekening

£ 5,97 /maand

-

Voor uw dagelijkse uitgaven krijgt u met deze rekening meer waar voor uw geld. Als u regelmatig overschrijvingen doet en geld opneemt, is Premium een goede keuze. Cashback, kortingen en alles wat u nodig hebt om gemakkelijk uitgaven te doen.

-

Voor uw dagelijkse uitgaven krijgt u met deze rekening meer waar voor uw geld. Als u regelmatig overschrijvingen doet en geld opneemt, is Premium een goede keuze. Cashback, kortingen en alles wat u nodig hebt om gemakkelijk uitgaven te doen.

Premium Plus

Hoofdaccount

£9.97 /maand

-

Als u een rekening nodig hebt voor uw loon en uitkeringen, voor het instellen van automatische betalingen of om contant geld te storten, dan is Premium Plus de beste keuze. Geniet van alle voordelen, voorrang in de wachtrij bij de klantenservice en maximale beloningen. Het ideale, zorgeloze alternatief voor een gewone bank voor uw hoofdrekening.

-

Als u een rekening nodig hebt voor uw loon en uitkeringen, voor het instellen van automatische betalingen of om contant geld te storten, dan is Premium Plus de beste keuze. Geniet van alle voordelen, voorrang in de wachtrij bij de klantenservice en maximale beloningen. Het ideale, zorgeloze alternatief voor een gewone bank voor uw hoofdrekening.

Voor wie is een schuldhulpverleningsplan geschikt?

Een DMP is doorgaans geschikt voor mensen die een vast inkomen hebben, maar moeite hebben om de minimale maandelijkse aflossingen voor meerdere schulden te betalen. Het werkt het beste bij ongedekte schulden en wordt meestal overwogen wanneer de schulden nog beheersbaar genoeg zijn om geen formelere insolventieoplossing, zoals een IVA of faillissement, te vereisen.

Hoe lang duurt een schuldhulpverleningsplan?

De looptijd van een schuldherschikkingsplan hangt af van het totale verschuldigde bedrag en van wat u realistisch gezien maandelijks kunt aflossen. De meeste plannen hebben een looptijd van één tot tien jaar, hoewel sommige mensen hun plan eerder afronden als hun financiële situatie verbetert of als ze een eenmalige uitkering ontvangen om hun schulden vervroegd af te lossen.

Heeft een schuldhulpverleningsplan invloed op mijn kredietwaardigheid?

Ja. Een schuldherschikkingsregeling heeft doorgaans een negatieve invloed op uw kredietwaardigheid, aangezien u uw schulden tegen een lager tarief aflost in plaats van volgens de oorspronkelijk overeengekomen voorwaarden. Deze informatie blijft zes jaar in uw kredietdossier staan. Voor veel mensen weegt de verbetering van hun financiële stabiliteit echter zwaarder dan de kortetermijngevolgen voor hun kredietwaardigheid.

Moet ik van bankrekening veranderen als ik een schuldhulpverleningsplan start?

Het wordt ten zeerste aangeraden om een nieuwe bankrekening te openen voordat uw schuldherschikkingsregeling ingaat. Als u bankiert bij een instelling waaraan u ook geld verschuldigd bent – bijvoorbeeld vanwege een rekening-courantkrediet of een creditcard bij dezelfde bank – heeft deze instelling het wettelijke recht om geld van uw lopende rekening te gebruiken om uw schuld bij hen te verrekenen. Dit staat bekend als het recht op verrekening, en het kan ertoe leiden dat u geen geld meer overhoudt voor essentiële kosten van levensonderhoud.

Waar moet ik op letten bij het kiezen van een bankrekening als ik een schuldhulpverleningsregeling volg?

Je hebt een rekening nodig zonder kredietfaciliteit, zonder gekoppelde kredietproducten en zonder verbanden met je huidige schuldeisers. Idealiter ondersteunt deze rekening automatische incasso’s en doorlopende opdrachten, zodat je je vaste rekeningen en betalingen in het kader van een schuldherschikkingsplan soepel kunt regelen. Het is ook de moeite waard om te zoeken naar rekeningen waarvoor geen kredietcontrole nodig is, aangezien je kredietwaardigheid tijdens een schuldherschikkingsplan waarschijnlijk onder druk komt te staan.

Kan ik tijdens een schuldherschikkingsregeling nog steeds een bankrekening openen als ik een slechte kredietwaardigheid heb?

Ja. Er zijn verschillende aanbieders die rekeningen aanbieden die speciaal zijn bedoeld voor mensen met een slechte kredietgeschiedenis. Deze worden soms ‘basisbankrekeningen’ of alternatieven voor bankrekeningen genoemd, zoals Suits Me. Ze voeren doorgaans geen kredietcontroles uit, dus je schuldherschikkingsplan of kredietwaardigheid zal geen belemmering vormen voor je aanvraag.

Heeft het overstappen naar een andere bank invloed op mijn schuldhulpverleningsplan?

Nee. Het openen van een nieuwe bankrekening heeft geen invloed op uw schuldherschikkingsregeling zelf. Uw schuldherschikkingsregeling blijft uw aflossingen volgens afspraak beheren. U hoeft alleen uw werkgever uw nieuwe bankgegevens door te geven voor de uitbetaling van uw loon, en eventuele automatische incasso’s of doorlopende opdrachten aan te passen aan uw nieuwe rekening.

Kunnen schuldeisers tijdens een schuldherschikkingsregeling nog steeds contact met mij opnemen of rente in rekening brengen?

Een DMP is een informele overeenkomst, dus schuldeisers zijn wettelijk niet verplicht om de rente te bevriezen of geen contact meer met u op te nemen. Veel schuldeisers zullen hier echter mee instemmen zodra er een regeling is getroffen. Een gerenommeerde DMP-aanbieder zal namens u onderhandelen om te proberen de rente en kosten op te schorten.

Moet ik kiezen voor een gratis of een betaalde DMP-aanbieder?

Gratis DMP-aanbieders zoals StepChange en Citizens Advice bieden dezelfde dienst aan als betaalde aanbieders, zonder dat het u iets kost. Als u voor een gratis aanbieder kiest, gaat een groter deel van uw geld naar het aflossen van uw schulden in plaats van naar kosten. Over het algemeen wordt aangeraden om een gratis, door de FCA gereguleerde aanbieder te kiezen.